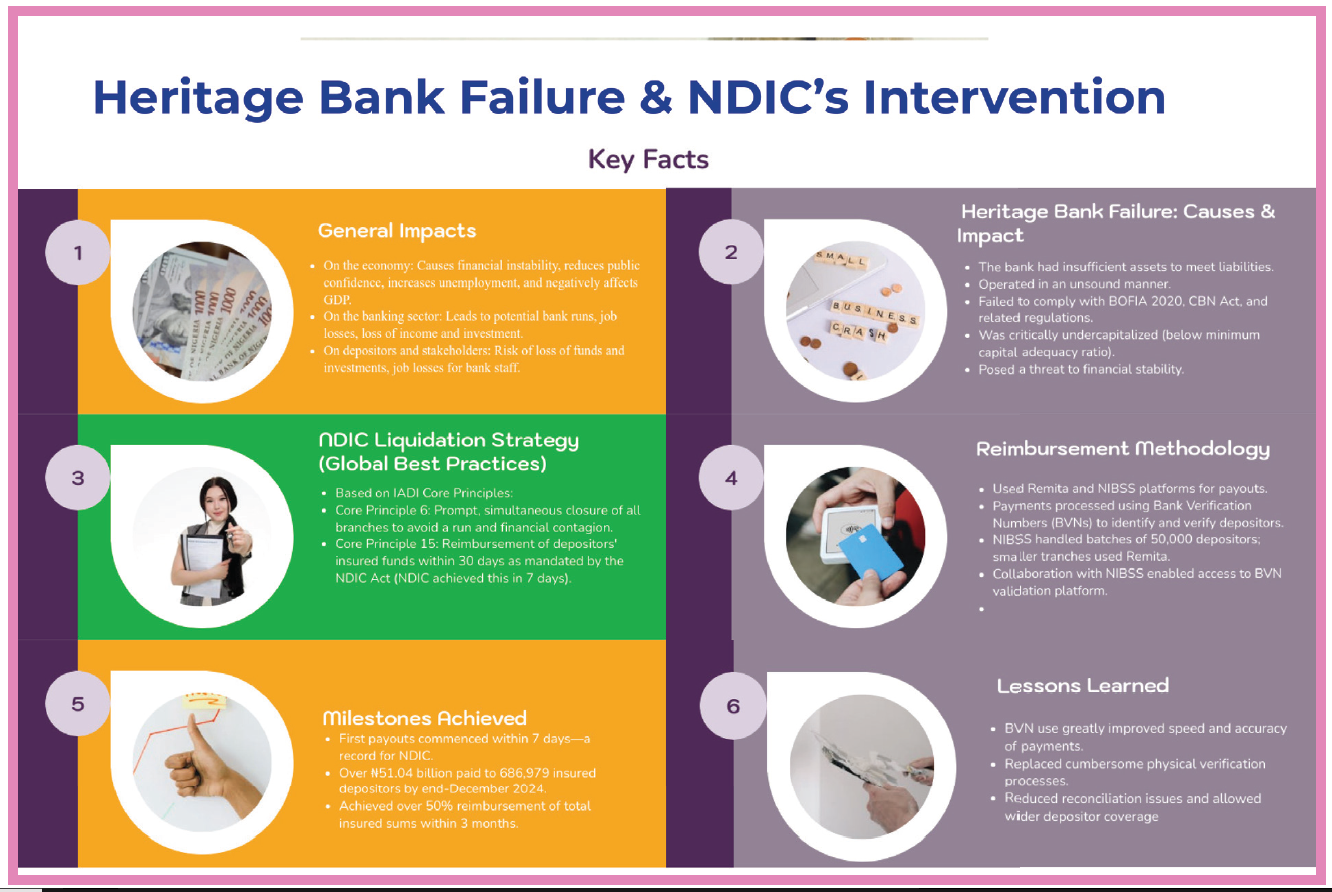

In a year marked by bold regulatory actions and reform-focused oversight, the Nigeria Deposit Insurance Corporation (NDIC) demonstrated its critical role in safeguarding Nigeria’s financial ecosystem following the closure of Heritage Bank Plc in June 2024. The bank’s collapse, attributed to severe regulatory violations and insolvency, prompted a fast and coordinated response from the NDIC, setting a new benchmark for liquidation efficiency in the banking sector.

The Central Bank of Nigeria (CBN) revoked Heritage Bank’s licence after it was discovered that the institution was critically undercapitalized, operated in an unsound manner, and had consistently failed to meet obligations outlined in the Banks and Other Financial Institutions Act (BOFIA) 2020 and the CBN Act. With a loan portfolio exceeding N700 billion and total deposits of about N650 billion, the failure posed a significant risk to public confidence, especially among its 2.3 million depositors.

Minimizing Panic, Upholding Global Best Practices

In alignment with the International Association of Deposit Insurers (IADI) Core Principles, the NDIC moved quickly to contain the fallout. The bank was closed simultaneously across all branches to prevent panic withdrawals and systemic contagion. Within three days – far below the 30-day statutory deadline stipulated by the NDIC Act No 30 of 2023 – the corporation commenced the reimbursement of insured deposits, leveraging digital tools and a data-driven approach that reflected best global practices.

The use of the Nigeria Inter-Bank Settlement System (NIBSS) and Remita platforms allowed the NDIC to disburse payments efficiently, using Bank Verification Numbers (BVNs) to validate depositor identities and account ownership. This innovative strategy eliminated the traditional need for physical verification, expediting the claims process and improving transparency.

Milestones Achieved, Lessons Learned

By the end of December 2024, the NDIC had paid N51.04 billion to 686,979 insured depositors—over half of the total insured sums owed. This unprecedented milestone not only highlighted operational improvements but also reinforced trust in the deposit insurance system.

One key lesson learned was the value of BVN integration, which significantly reduced the time and cost associated with reimbursements. Unlike previous liquidations that required manual verification and in-house disbursements, the BVN-linked model enabled seamless digital payments, improved reconciliation, and minimized errors.

Next Level of NDIC’s Performance

The corporation took its ground-breaking performance to the next level when it commenced payment of liquidation dividends to depositors of the defunct Heritage Bank from the proceeds of the bank’s assets sales and recovery of debts on Friday 25th April, 2025, less than one year after the revocation of the bank’s licence. In a statement signed by Ag. Head, Communication and Public Affairs, Hawwau Gambo, NDIC had declared a staggering N46. 6 billion as first tranche liquidation dividend to be paid to depositors whose balances in the failed bank exceeded the maximum insured limit of N5 million at the rate of 9.2 kobo per naira on a pro-rata basis. The statement said the dividend payment underscored the corporation’s commitment to ensuring that depositors of the defunct Heritage Bank are fully reimbursed without undue delay.

This is particularly profound and unprecedented considering the bitter experience of prolonged delay often experienced by depositors while the corporation grappled with daunting legal and procedural hurdles that debtors characteristically cast into the wheel of bank liquidation.

Beyond Heritage Bank: Broader Initiatives in 2024

Outside of Heritage Bank’s liquidation, the NDIC made notable strides during the year. It declared liquidation dividends for uninsured depositors and creditors of Liberty Bank, Fortis Microfinance Bank, and Allstates Trust Bank. The Corporation also intensified its Deposit Tracer Initiative, focusing on unverified government depositors, particularly Ministries, Departments, and Agencies (MDAs), to ensure outstanding payments through the Treasury Single Account (TSA) system.

Furthermore, capacity building for staff in liquidation management remained a strategic focus, equipping personnel with up-to-date tools and knowledge for handling future bank failures more efficiently.

Bank failures, while unfortunate, are not without economic consequences—ranging from reduced GDP and job losses to loss of depositor funds and investor confidence. However, NDIC’s swift and structured response to Heritage Bank’s collapse reaffirmed its institutional readiness and the robustness of Nigeria’s bank resolution framework.

As financial systems face increasing pressure from global uncertainties and domestic challenges, NDIC’s achievements in 2024 serve as a model for how deposit insurers can protect depositors, stabilize the economy, and build long-term confidence in the banking sector.

Transformative Strategies in Asset Recovery

Through strategic foresight, robust legal backing, and seamless coordination, the corporation—via its Asset Management Department (AMD)—has showcased a new paradigm in financial sector crisis management beyond the defunct Heritage Bank to the other banks in-liquidation, particularly the closed 49 Deposit Money Banks (DMBs)

At the heart of NDIC’s accomplishments lies the implementation of comprehensive debt recovery strategies that span loan restructuring, borrower engagements, litigation, garnishee proceedings, and foreclosure actions. These were further strengthened by the adoption of technology and digitization of asset records, which enhanced transparency, tracking, and efficient valuation processes.

Through proactive partnerships with external professionals such as Debt Recovery Agents (DRAs), Solicitors, Auctioneers, and Property Valuers, NDIC was able to widen its asset realization net. These strategic alliances not only improved turnaround time but also boosted recovery outcomes. Critical to this was the deployment of an internal control framework that ensured adherence to corporate governance, risk management, and compliance policies.

Boosting Payment with Impressive Asset Recovery Performance

The paradigm shift in asset management has given remarkable boost to the ability of the NDIC to pay liquidation dividends to depositors of the 50 DMBs in-liquidation, thereby increasing public confidence in the banking system. NDIC had paid cumulative sum of N105.766 billion to the uninsured depositors, N1.285 billion to 1,039 creditors, and N4.899 billion to 1,007 shareholders of the DMBs as at 31st March 2025. More profoundly, 100 percent liquidation dividend had been declared to depositors of 16 DMBs in-liquidation.

NDIC Act 2023: A Game-Changer in Liquidation Operations

The signing of the NDIC Act No. 33 of 2023 by former President Muhammadu Buhari on May 26 significantly transformed the legal and operational framework of the corporation. The Act endowed NDIC with enhanced powers that now form the bedrock of its asset recovery and liquidation success.

The NDIC, through the operational excellence of its AMD, has proven its readiness to manage crises, restore confidence, and recover value from failed institutions. The success story of Heritage Bank’s resolution demonstrates how strategic foresight, a responsive legal framework, and operational agility can redefine financial sector resilience.