By Jennete Ugo Anya

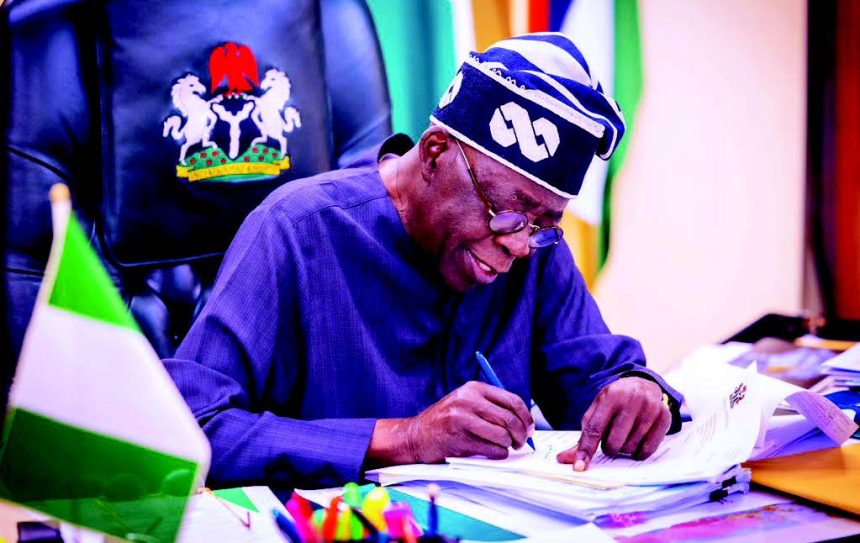

A new chapter in Nigeria’s fiscal history quietly began at the Presidential Villa last Thursday as President Bola Tinubu signed four major tax reform bills into law. A move the presidency says will reshape the country’s tax landscape, improve ease of doing business, and drive both revenue and investment growth.

While the signing ceremony itself was short and formal, its significance is far-reaching. It was attended by a powerful mix of political and economic actors, which included the Senate President, Speaker of the House of Representatives, federal lawmakers, governors, key ministers, and presidential aides.

The four laws: the Nigeria Tax Bill, Nigeria Tax Administration Bill, Nigeria Revenue Service (Establishment) Bill, and Joint Revenue Board (Establishment) Bill – are products of months of debate, consultation, and controversy. They were initially greeted with skepticism from some quarters, particularly from state governors who feared potential fiscal strain. Some even argued that certain provisions could leave states unable to pay salaries.

But the federal government held its ground. According to presidential spokespersons, extensive consultations were held with key stakeholders across the federation to address these concerns. And with last Thursday’s assent, the administration is signaling that it is ready to follow through on its promise of deep-rooted reforms.

Speaking after the event, Dr. Zacch Adedeji, Chairman of the Federal Inland Revenue Service (FIRS), announced that the new tax regime would officially take effect on January 1, 2026. He explained that the extended lead time is not just a grace period, but a strategic window for full-scale sensitisation and system restructuring. “It takes time for all stakeholders – operators, regulators, and participants – to transition to a new tax system. We now have six full months to prepare the ecosystem, not in the media space, but in the real systems that support this reform,” Dr. Adedeji told the media.

Each of the four bills carries a distinct but interconnected function. The Nigeria Tax Bill seeks to harmonise Nigeria’s fragmented tax codes into a more unified, streamlined system; reducing duplication and easing compliance. The Tax Administration Bill provides a standardised legal and operational framework across federal, state, and local tax systems.

Perhaps most transformative is the Nigeria Revenue Service (Establishment) Bill, which dissolves the Federal Inland Revenue Service (FIRS) and replaces it with a more autonomous, performance-driven agency – the Nigeria Revenue Service (NRS). This new body will be tasked not only with collecting taxes but also managing non-tax revenue and enforcing higher standards of transparency and accountability.

The fourth law, the Joint Revenue Board (Establishment) Bill, is aimed at fostering cooperation between tax authorities across the three tiers of government, providing a governance structure for policy alignment and data sharing — a step many experts believe is long overdue.

Economists and policy analysts say the combined effect of these reforms, if well implemented, could provide Nigeria with a more predictable tax environment, reduce informal sector leakages, and make the country more attractive to foreign investors. Yet, as with all reforms, the real test lies ahead; in execution, communication, and political will.

Despite the pushback that trailed the early stages of the bills, the administration seems determined to stay the course. For President Tinubu, who has consistently emphasised fiscal discipline and revenue expansion since assuming office, this tax overhaul is more than policy – it is a signal of intent.

FIRS Backs Voluntary Tax Compliance With Tech-Driven Reform

Meanwhile, the FIRS is overhauling Nigeria’s tax system with a renewed focus on voluntary compliance, technology adoption, and taxpayer education.

The new strategy shifts away from heavy reliance on punitive audits toward a model that makes tax compliance simpler and more intuitive. “Our goal is not just enforcement; it is enablement,” the service said.

Central to the reform is the deployment of predictive technologies that detect risks early, streamline processes, and support real-time interactions with taxpayers. These innovations are backed by standardised operating procedures to ensure consistency and clarity.

Rather than act as a watchdog, FIRS is positioning itself as a partner in national development- investing in public awareness and training programs for both staff and citizens to build tax literacy. “This transformation is powered by purpose. We are raising revenue in ways that are efficient, equitable, and empowering,” Dr. Adedeji noted.

The reform supports Nigeria’s broader fiscal goals of boosting internally generated revenue, improving transparency, and reducing dependence on borrowing. In promoting trust and shared responsibility, FIRS aims to create a future where audits are secondary to sustained, voluntary compliance.