For decades, conversations about Africa’s economic future were often framed around debt relief, foreign aid, and development assistance. At major global conferences, African leaders frequently sought concessional financing, humanitarian support, or external interventions to address economic instability and infrastructure gaps.

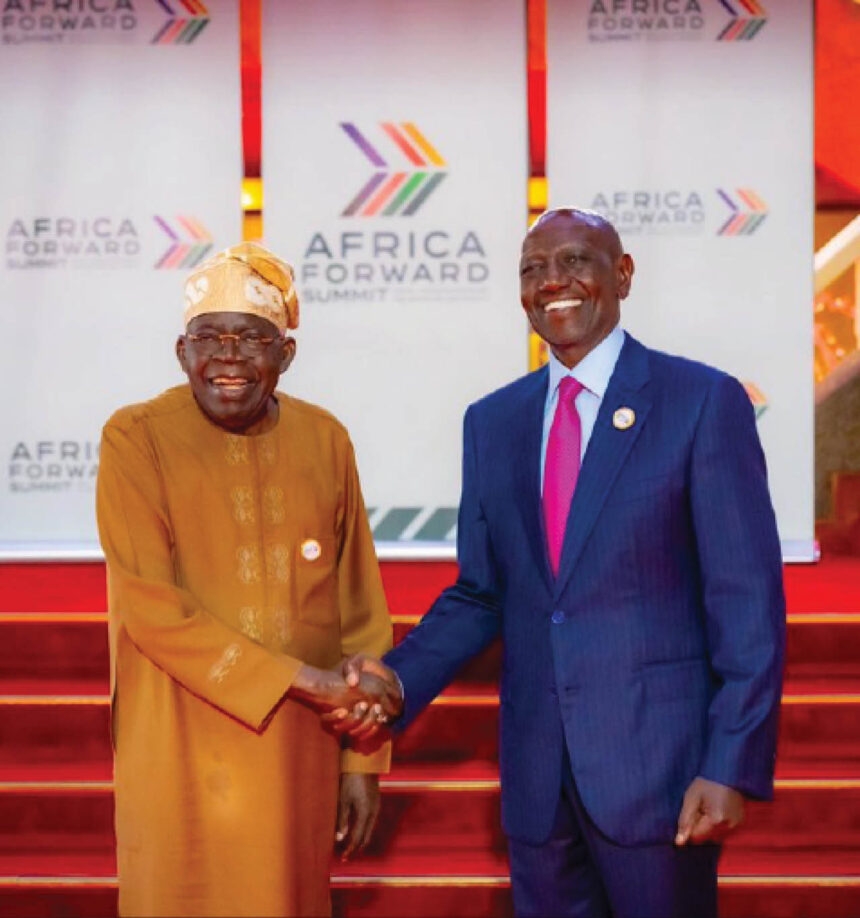

But a different tone emerged at the recent Africa Forward Summit in Nairobi, Kenya, where political leaders, policymakers, financiers, and business executives presented a more assertive economic argument centred on financial sovereignty, industrial growth, domestic capital mobilisation, and investment-driven partnerships. Enam Obiosio discusses the highlights of the summit.

The summit brought together a range of influential voices, including President Bola Ahmed Tinubu of Nigeria, Kenyan President, William Ruto, Honourable Minister of Finance and Coordinating Minister of the Economy, Taiwo Oyedele, senior policymakers, international investors, and multinational business operators. Their discussions reflected a broader continental effort to redefine how Africa finances development and positions itself within the global economy.

Rather than focusing primarily on dependency-driven development models, the summit conversations increasingly revolved around industrial execution, productive investment, domestic savings, infrastructure financing, and regional economic competitiveness.

At the heart of the discussions was a growing concern among African governments that the continent’s industrial ambitions continue to face structural obstacles linked to high borrowing costs, restrictive financing systems, and dependence on externally priced capital.

Taiwo Oyedele argued that Africa’s financing environment remains heavily shaped by what he described as “unfair risk assessment” and a “prejudice premium,” conditions he said continue to limit access to affordable long-term capital for productive investment.

According to him, the summit repeatedly returned to the question of how Africa could industrialise effectively while remaining constrained by financing structures that make capital significantly more expensive for African economies than for many other parts of the world.

Oyedele stated that Africa continues to face “high borrowing costs,” “restrictive financing terms,” “limited access to long-term capital,” and “inadequate financing for productivity and value addition.”

His comments reflected wider frustrations across the continent over sovereign risk assessments and international financing conditions that many African policymakers believe do not accurately reflect the region’s demographic potential, investment opportunities, and expanding consumer markets.

He also argued that Africa’s financing priorities must evolve beyond systems largely focused on raw material extraction and emergency interventions.

“Financing priorities must shift from merely extracting raw materials and funding emergencies to enabling value addition, infrastructure, skills development, regional value chains, technology and innovation,” Oyedele said.

The summit’s discussions highlighted how the debate around economic transformation in Africa is increasingly moving toward questions of industrial productivity and internal capital formation.

President William Ruto expanded the conversation into a broader discussion about sovereignty and long-term self-financing, insisting that Africa’s future could no longer remain dependent on aid-driven development systems and unsustainable borrowing cycles.

“The age in which Africa’s development was principally framed through aid, dependency, and unsustainable borrowing must give way to a new paradigm grounded in investment, innovation, domestic resource mobilisation, and strategic partnerships built on sovereign equality and mutual benefit,” Ruto stated.

Ruto also emphasised the importance of domestic savings and pension assets in financing African development, pointing to the scale of financial resources already existing within the continent.

“Africa must increasingly finance Africa,” he said, noting that the continent possesses “more than $4 trillion in long term domestic savings, including over $1 trillion in pension and insurance assets.”

His advocacy for an African credit rating agency also reflected increasing continental interest in reducing reliance on external financial institutions that many governments believe contribute to elevated borrowing costs for African economies.

While much of the summit focused on financing structures and economic sovereignty, President Tinubu shifted attention toward commercial execution and investment delivery, using the platform of the 10th France-Nigeria Business Council Meeting to position Nigeria-France relations around infrastructure, manufacturing, logistics, and hospitality investments.

According to a State House statement signed by the Special Adviser to the President on Information and Strategy, Bayo Onanuga, the meeting also brought together leading business figures from both countries, including Aliko Dangote, Abdul Samad Rabiu, Tony Elumelu, Patrick Pouyanné of TotalEnergies, and Rodolphe Saadé of CMA CGM.

The gathering also produced a major hospitality agreement between Accor and Shoreline Group for what was described as Nigeria’s first national hotel platform, an initiative positioned as part of wider investment activity within the country’s services and tourism sectors.

President Tinubu described the project as “a major vote of confidence in Nigeria’s hospitality, tourism, services and investment future.”

More broadly, Tinubu presented Nigeria-France relations as entering what he called an “execution phase,” where diplomatic engagements would increasingly focus on commercially measurable outcomes tied to infrastructure development, industrial partnerships, and job creation.

“This is the partnership Nigeria is ready for. We are ready for investment that builds, capital that produces, and enterprise that creates jobs. Nigeria and France are no longer simply exchanging goodwill. We are opening a new chapter of serious economic execution,” Tinubu stated.

The summit also revealed growing alignment among African policymakers around several strategic economic priorities, including reducing dependence on externally priced capital, strengthening domestic investment ecosystems, expanding industrial production, and using regional partnerships to support long-term competitiveness.

Infrastructure, manufacturing, renewable energy, logistics, hospitality, agriculture, fintech, artificial intelligence, and technology emerged repeatedly during discussions as sectors expected to shape Africa’s next growth phase.

At the same time, participants acknowledged persistent structural risks confronting African economies, including sovereign debt pressures, foreign exchange instability, fragmented capital markets, regulatory inconsistencies, infrastructure deficits, and weak execution capacity.

The summit therefore reflected more than a routine policy conference. It highlighted a broader shift in the language of African economic leadership, from dependency toward competitiveness, from external rescue toward internal capital mobilisation, and from diplomatic symbolism toward commercially executable partnerships.

Whether those ambitions ultimately translate into measurable industrial expansion, stronger infrastructure systems, and sustainable economic transformation will depend largely on how effectively governments, financial institutions, and private-sector operators convert policy declarations into long-term investment execution across the continent.